Rental costs in England are some of the highest in Europe with those aged 16 to 24 spending more than 40% of their income on rent. Average rents now exceed £1,300 and over £2,600 in London.

While most tenants manage to pay their rent on time and in full, rising living costs add to the burden. A report by Citizens Advice also found that one in six tenants worried about being able to pay their rent and estimated that nearly one in ten were in arrears, owing an average of £937 each.

If you’re managing property, rent arrears is a challenge you’ll inevitably come across. If you offer a tenant-find service, it’s also likely to be a topic at the forefront of landlords’ minds.

Here, we look at what you can do to minimise the risk of rent arrears, how to resolve issues if they arise, and how you can protect your and your landlord’s income with rent guarantee insurance.

What are rent arrears?

Tenants are in rent arrears if they:

- Miss rental payments;

- Only make partial rental payments;

- Are late making rental payments.

Can we charge fees for late rental payments?

Yes. Your agency (or landlords) can charge interest for late rental payments but there are strict rules about how this is applied.

Under the Tenant Fees Act 2019, charges for late rent are classed as default fees (these apply if there’s been a breach of contract).

Interest can only be charged if rent is more than 14 days late from the usual due date set out in the tenancy agreement. The daily fee you charge cannot be more than 3% above the Bank of England’s base rate (anything more than this is illegal).

What can letting agencies do if tenants get into rental arrears?

Tenants can fall into arrears for any number of reasons; for example, they may have to cover an unexpected cost or are made redundant. However, tenancy agreements should be clear about what happens if rent is paid late or what happens if tenants default altogether.

Steps you can take to resolve the issue, include:

Discuss with the tenant

If a tenant misses a payment, it’s worth waiting three or four days to see whether it’s late or if there’s been a banking complication. Waiting any longer than this simply prolongs the issue.

If you call the tenant, it’s a good idea to follow up on any conversations you have in writing so there’s clarity about what you’ve discussed.

Tenants may respond quickly if the problem is short-term or there’s been an admin error when setting up bank payments.

Request for payment in instalments

If the difficulty is a short-term problem (such as waiting for a new job to start or having to cover a one-off payment elsewhere), a payment plan could be a straightforward solution. If this is the case, the tenant may agree to pay the outstanding rent over a few months.

If you’ve built a good relationship with tenants and suspect they may need more long-term support, you can also steer them towards free budgeting advice from debt charity StepChange and Citizens Advice.

Bear in mind that financial troubles can be difficult, embarrassing, and awkward to talk about, so it’s a topic that needs to be broached with care and understanding.

Send a formal letter

If you get no response from the tenant, the next step is to send them a formal letter. The letter should be professional and polite, clearly stating what it’s about (late rent payments). You should also include details of when rent was due and what might happen if it isn’t paid (court proceedings and eviction).

If you’re not sure how to go about this, consumer rights platform Which? has a handy template you can use for rent arrears.

Contact the guarantor

If tenants have a rent guarantor, you can contact them if tenants don’t reply to your letter or any other attempts at contacting them.

When guarantors co-sign tenancy agreements (or sign other contracts listing them as guarantors), they are legally obliged to follow any terms set out. If you need to contact them, you should let them know how much rent is outstanding and when it was due. You can also make it clear how they can make arrangements for it to be paid.

It’s worth reminding guarantors that failure to pay can result in court action. Which? also has a useful template you can use for rent guarantors.

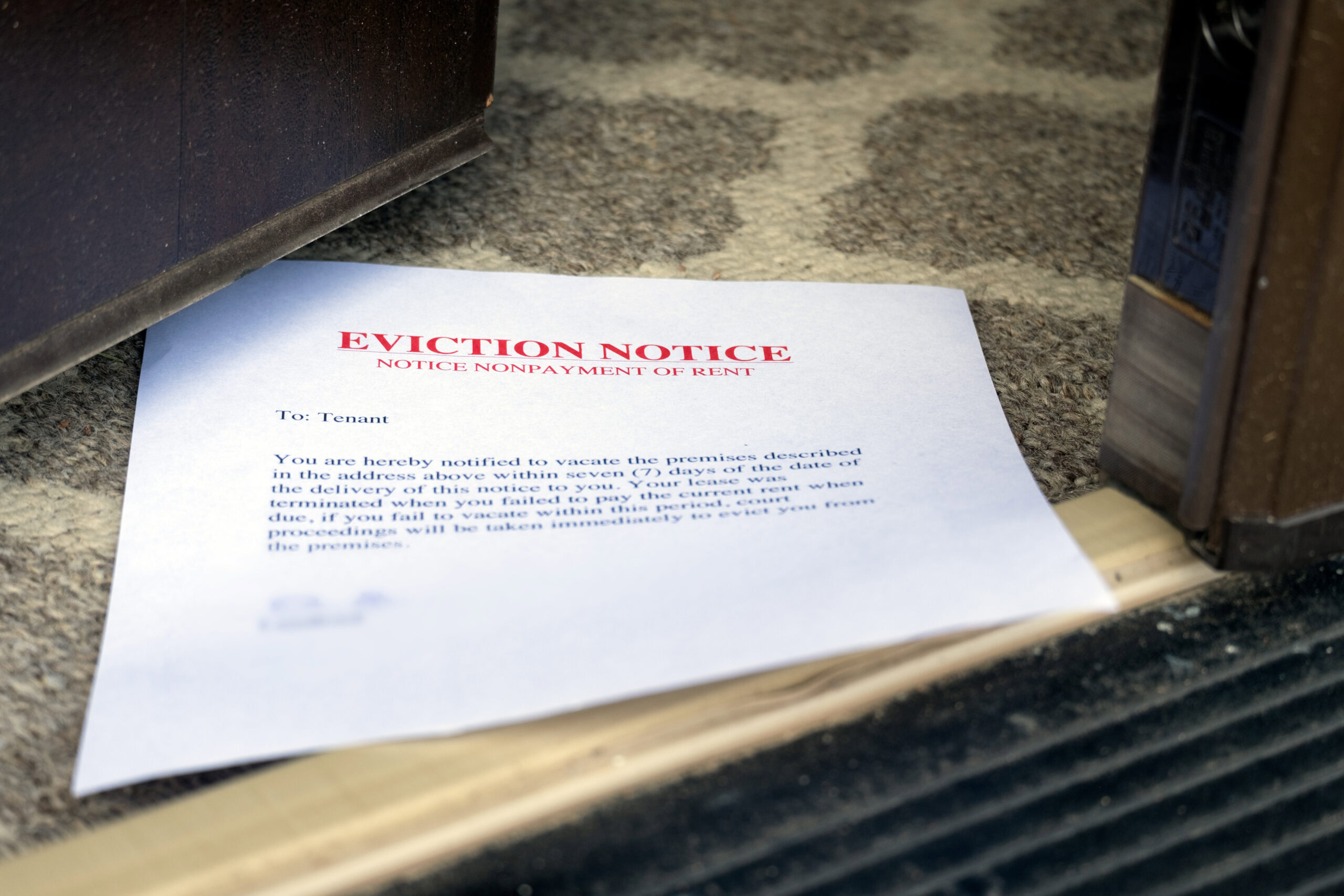

Begin the eviction process

Some situations cannot be easily resolved, and your final option is to start the eviction process. The eviction process you must follow will depend on the tenancy agreement and where your agency (and properties) are based.

The eviction processes below apply to assured shorthold tenancies (ASTs) in England. You can find the process for other areas at:

In England, if rent hasn’t been paid, you can serve tenants notice under Section 8 of the Housing Act 1988 which sets out a list of mandatory and discretionary grounds for eviction.

The terms of Section 8 list rent arrears as a mandatory reason for eviction (ground 8). You can only start the Section 8 eviction process if rent is:

- More than eight weeks late (if it’s due weekly or fortnightly);

- More than two months late (if paid monthly);

- More than three months late (if rent is paid quarterly or annually).

If you decide to start the eviction process, you must follow the correct procedure for it to be valid. If not, it can be rejected in court.

The first step in a Section 8 eviction, is to send tenants a notice seeking possession (NSP). This is notice that you intend to bring court proceedings against the tenant unless they leave the property by a specified date.

It’s worth noting that you can also serve the Section 8 notice under two discretionary grounds (these are less likely to lead to eviction but will be considered by courts); they are:

- Ground 10 – where rent arrears are less than in ground 8.

- Ground 11 – the tenant is persistently late in paying rent (the tenant doesn’t need to be in arrears at the time for this to apply).

Another option is to serve a Section 21 notice (a ‘no-fault’ eviction). This can only be used after the first four months of a tenancy. If the tenancy is fixed term, you can ask the tenant to leave at the end. If the tenancy has no fixed end date, you must give at least two months’ notice. However, at the time of writing this article, Section 21 notices are due to be abolished under the Renters’ Rights Bill.

If you want, you can serve a Section 8 and Section 21 notice at the same time.

Bring eviction proceedings

If tenants do not leave the property by the date in your notice seeking possession, you’ll need to apply for a possession order.

This is a formal notice from the court that the tenant must leave the property by a certain date. A court-appointed bailiff can enforce the eviction if they still don’t leave. For more details about the process and what you’ll need to do, take a look at our guide: How do you evict a tenant?

Can tenants withhold rent?

Tenants are strongly advised not to withhold rent. However, in some cases, tenants may feel they have no choice but to withhold rent if landlords fail to meet their responsibilities and keep the property safe and habitable.

Examples of when they may choose to do this include if they have to repair damage they didn’t cause (such as repairs to fences or windows because of a storm or vandalism). If tenants decide to withhold rent, they should always let you know why first.

You can avoid this by ensuring that you meet all landlord obligations for the properties you manage.

How far back can we claim rent arrears?

You can claim for up to six years after the money is due. As long as you have the tenant’s new address, you can go to the Small Claims Court and get a County Court Judgement for the arrears. You then have six years to enforce the CCJ.

If the tenant doesn’t pay, you can get it enforced by a County Court Bailiff who can take the tenant’s personal belongings and sell them. Alternatively, you can ask a court for an Attachment of Earnings Order. This will deduct payments from the tenant’s wages or benefits.

However, this is a long and expensive process with no guarantee your agency (or landlord) will get any rent arrears back.

How can rent guarantee insurance help with rent arrears?

Rent guarantee insurance covers rental payments if tenants and their guarantors fail to pay. You can choose to buy a policy for the properties you manage (protecting your agency management fees) or refer landlords to the service.

Policies with Alan Boswell Group compensate you up to £5,000 in rental income per month and offer up to 15 months’ rental cover. We can also provide 75% of the monthly rent for up to three months after an eviction. Legal expenses cover is also included to help you with the eviction process.

You can find out more about rent guarantee insurance and the peace of mind it can offer you and your landlords, by calling us on 01603 649727.

FAQs

How can we prevent rental arrears in the first place?

While it’s impossible to guarantee a tenant won’t fall into arrears, you can take steps to make it less likely. We’d always recommend thorough tenant referencing before agreeing a tenancy. Comprehensive referencing should highlight any issues with credit and stress test affordability.

Asking for the rent to be paid by direct debit or standing order can also encourage tenants to ensure there’s enough money to meet their rent when it’s due.

Is it worth getting rent guarantee insurance or a rent guarantor?

If you’re considering asking tenants for rent guarantors (or your landlords show preference for this), remember that guarantors can also default. In contrast, rent guarantee insurance will pay out as long as you’ve fulfilled any conditions in the policy.

You can still choose rent guarantee insurance if your tenants also have a guarantor (in which case, the insurer will also pursue a guarantor for rent, if appropriate).

Can I evict a tenant immediately for non-payment?

Not normally. Tenants generally have to be at least eight weeks in arrears before you can start proceedings. However, if a tenant is persistently late in paying rent, you could start the eviction process according to Ground 11 of Section 8. As it’s a discretionary ground, there’s no guarantee an eviction would be successful.

Information provided in this article was correct at the time of publication. This article is intended as a guide only. Please note that legislation does change, it is always best to check the most up to date guidance on gov.uk.